What Is an Off-Plan Property Mortgage in Dubai?

An off-plan property mortgage in Dubai is a specialized type of home loan provided by UAE banks to finance the purchase of a property that is still under construction. Unlike mortgages for ready or completed properties, off-plan mortgages are structured around the development timeline, meaning that funds are released in stages as the project reaches certain construction milestones—usually when 50–60% of the construction is completed. This staged approach ensures that both the buyer and the bank are protected throughout the development process.

Key Features of Off-Plan Mortgages

-

Linked to Construction Milestones: Funds are disbursed progressively according to the project’s completion stages, which allows buyers to manage cash flow efficiently.

-

Direct Disbursement to Developers: The bank pays the developer directly, ensuring that payments are secure and aligned with construction progress.

-

Lower Initial Cash Requirements: Buyers often need to pay only 10–20% upfront, making it easier to enter premium developments without large immediate capital outlay.

-

Ideal for Long-Term Investors: Off-plan mortgages are particularly attractive for investors seeking capital appreciation over time, as they can secure units at launch-stage prices before the property market value increases.

Many leading developers in Dubai offer off-plan projects eligible for bank financing, including Emaar, Damac, Sobha, Nakheel, Meraas, Danube, Binghatti, and several others. Choosing an approved developer not only simplifies the mortgage approval process but also reduces risks associated with construction delays or project cancellations.

Off-plan mortgages have become a cornerstone of Dubai’s property investment landscape, combining financial flexibility with the potential for high returns, making them an essential option for anyone looking to enter the city’s real estate market strategically.

Why Consider an Off-Plan Mortgage in Dubai?

Investing in off-plan property in Dubai offers several advantages, particularly when combined with a mortgage. Buyers can enjoy financial flexibility, reduced upfront costs, and the potential for significant long-term returns. Here’s why an off-plan mortgage is an attractive option for investors and homebuyers alike:

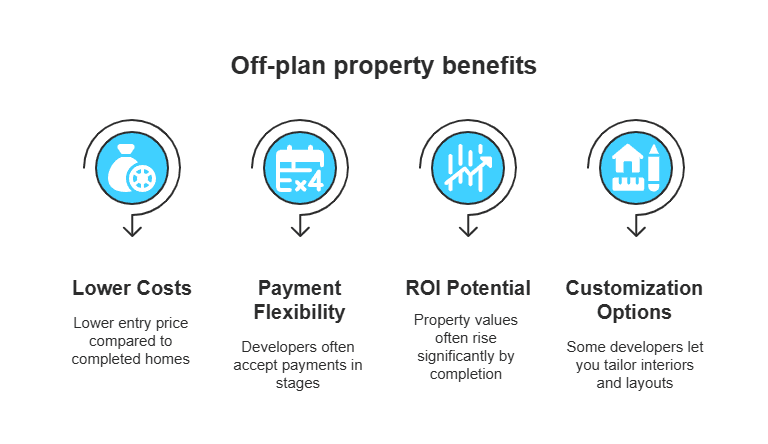

1. Lower Entry Price

Off-plan properties are typically 10–25% cheaper than ready or completed homes. This allows investors to secure a premium property at launch-stage prices, gaining access to desirable locations and high-quality developments at a more affordable cost. Early investment also increases the potential for capital appreciation as the project nears completion.

2. High Capital Appreciation

Dubai’s real estate market has a strong track record of price growth during construction phases. Buying off-plan allows investors to benefit from early equity gains between the launch and handover periods. This makes off-plan investments particularly attractive for long-term portfolio growth and wealth accumulation.

3. Flexible Payment Plans

Developers in Dubai offer a variety of construction-linked payment plans designed to reduce financial pressure on buyers. Common structures include:

-

Post-handover payment plans

-

60/40 or 70/30 split plans

-

Stage-wise installments linked to construction milestones

4. Leverage Financing

Using an off-plan mortgage allows buyers to pay a portion of the property cost upfront while financing the remainder over several years. This financial leverage maximizes long-term returns on investment, allowing investors to acquire premium properties without tying up all their capital at once.

5. Ideal for First-Time Buyers

Off-plan mortgages lower the entry barriers for new investors and first-time homebuyers. With smaller monthly payments, structured installments, and access to modern, future-ready communities, off-plan financing makes it easier for newcomers to participate in Dubai’s booming property market.

Who Should Choose an Off-Plan Mortgage?

An off-plan property mortgage in Dubai is a versatile financing solution that caters to a wide range of buyers. Whether you are a first-time homebuyer, a long-term investor, or an expatriate looking to enter the UAE property market, off-plan mortgages offer financial flexibility and strategic advantages. Here’s a detailed look at who can benefit most:

1. First-Time Home Buyers

Off-plan mortgages are particularly attractive to first-time buyers who may not have large capital reserves. They benefit from:

-

Affordable initial payments, often as low as 10–20% of the property value

-

Long-term repayment plans, spreading costs over construction and beyond

-

Access to new communities, allowing them to choose premium locations and modern amenities

2. Long-Term Investors

For investors focused on capital growth, off-plan properties offer significant advantages:

-

Capital appreciation between launch and handover stages

-

High rental yields after project completion

-

Low maintenance costs, as new units are covered under warranties and equipped with modern systems

3. End Users Planning for the Future

Buyers intending to move into their property within 1–3 years find off-plan mortgages ideal. By the time construction is completed, they can occupy their new home with minimal financial strain, while also benefiting from lower initial purchase prices.

4. Buyers with Limited Upfront Capital

Off-plan financing allows buyers to pay only a portion of the property during construction—often 50%—while securing a mortgage for the remainder. This enables access to premium projects without tying up all available funds, making high-value properties more accessible.

5. Expatriates Seeking Secure Entry into UAE Real Estate

For expatriates, off-plan mortgages provide a safe and structured entry point into the Dubai property market. By working with bank-approved developers and reputable projects, expats can reduce investment risk while taking advantage of Dubai’s tax-free property benefits and high potential returns.

When Should You Apply for an Off-Plan Mortgage?

Timing plays a crucial role when applying for an off-plan property mortgage in Dubai. Unlike ready properties, banks only approve and disburse mortgages for off-plan projects once certain conditions are met. Understanding these requirements ensures a smoother approval process and helps buyers maximize financial benefits.

Bank Approval Requirements

Banks typically approve off-plan mortgages only when:

-

Project Reaches 50–60% Completion: Banks require a significant portion of the property to be constructed to reduce project risk and ensure timely completion.

-

Developer and Project Are Bank-Approved: Only developers on the bank’s approved list are eligible for mortgage financing, ensuring credibility and reliability.

-

Buyer Has Paid an Initial Amount: Usually, the buyer must pay 40–50% of the property price upfront, which demonstrates financial commitment and reduces the bank’s exposure.

Ideal Timing to Apply

For maximum benefits, consider applying for an off-plan mortgage:

-

During Mid-Construction: Applying around the halfway point of construction ensures the project meets bank milestone requirements while keeping upfront payments manageable.

-

When Ready to Lock in Interest Rates: Securing a mortgage early allows buyers to lock in favorable fixed or variable interest rates, potentially saving money over the long term.

-

When EIBOR Rates Are Stable: Since most Dubai mortgages are tied to the Emirates Interbank Offered Rate (EIBOR), stable rates reduce the risk of higher repayments on variable mortgages.

Where to Buy Off-Plan Property in Dubai?

Dubai offers a wide range of off-plan property opportunities, catering to investors and end-users alike. Choosing the right location and developer is crucial, as banks only approve mortgages for projects built by reputable developers with strong completion track records. Investing in well-established communities not only ensures smoother mortgage approvals but also enhances the potential for capital appreciation and rental returns.

Top Off-Plan Communities in Dubai

Some of the most sought-after off-plan communities with high mortgage approval rates include:

-

Dubai Hills Estate: A master-planned community featuring luxury villas, apartments, and townhouses surrounded by green spaces and golf courses.

-

Emaar Beachfront: Premium waterfront apartments offering direct access to pristine beaches and a vibrant lifestyle.

-

Downtown Dubai: Iconic residences near the Burj Khalifa and Dubai Mall, combining luxury living with strong rental demand.

-

Business Bay: Ideal for professionals and investors, with a mix of commercial and residential properties in Dubai’s central business hub.

-

Jumeirah Village Circle (JVC): Affordable and family-friendly community with modern villas and apartments.

-

Dubai Creek Harbour: Waterfront living with luxury apartments, commercial spaces, and panoramic views of Dubai Creek.

-

Meydan: Known for upscale villas and apartments in a serene community with sports and leisure facilities.

-

Palm Jebel Ali (New Projects): Exclusive island developments offering luxury waterfront living with long-term investment potential.

-

Arabian Ranches 3: Family-focused community with spacious villas, landscaped gardens, and modern amenities.

-

Damac Lagoons: Resort-style residential community with themed villas and world-class recreational facilities.

Why Location Matters

Banks and developers prioritize projects in reputable locations with proven demand and growth potential. Investing in these communities ensures:

-

Higher chance of mortgage approval

-

Better rental yields after handover

-

Strong capital appreciation over time

-

Access to premium amenities and lifestyle facilities

Selecting the right off-plan project in Dubai is a critical step toward a successful real estate investment. Always verify that the developer is bank-approved and has a history of timely project delivery to safeguard your investment and mortgage approval process.

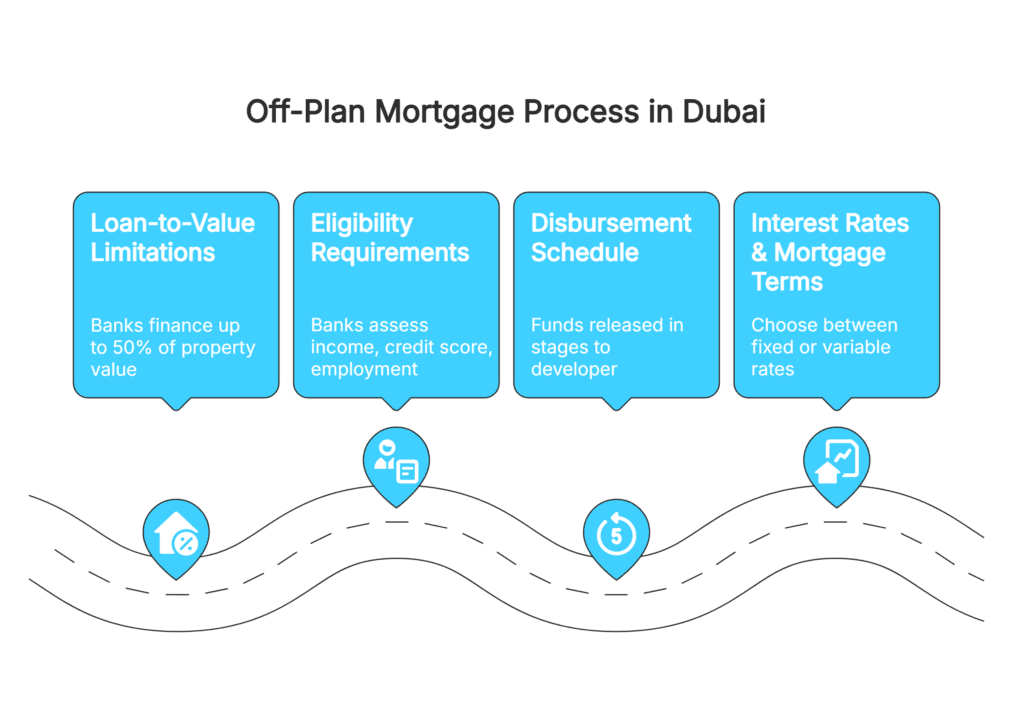

How Do Off-Plan Mortgages Work? (Step-by-Step)

Understanding the step-by-step process of off-plan mortgages is essential for buyers and investors looking to enter Dubai’s property market. Off-plan financing works differently from ready-property loans, as it is closely linked to the project’s construction stages and developer milestones. Here’s a detailed breakdown:

1. Book the Unit

The process begins by selecting your preferred off-plan property and paying an initial booking amount, usually 10–20% of the property value, directly to the developer. This confirms your intent to purchase and reserves the unit.

2. Make Construction-Based Payments

Developers in Dubai follow construction-linked payment plans, which break the property price into multiple stages. Typical payments may include:

-

10% at booking

-

10% after 6 months

-

10% when 20% of construction is completed

-

Further installments tied to subsequent milestones

These staged payments reduce upfront financial burden while ensuring progress-based investment.

3. Apply for the Mortgage

Once the initial payment is made and the project reaches bank-required milestones, buyers submit their mortgage application. The bank evaluates:

-

Income and employment stability

-

Credit score (AECB for expats and UAE nationals)

-

Project and developer approval status

-

Construction progress

This ensures the bank’s risk is minimized while confirming the buyer’s repayment capability.

4. Bank Valuation

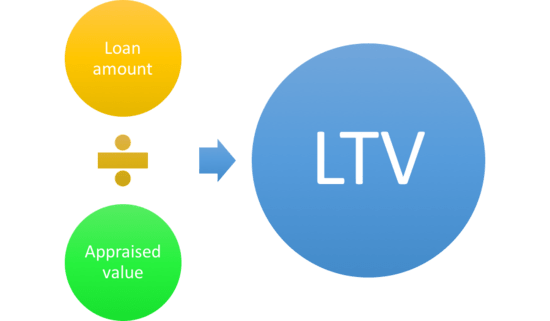

After reviewing the application, the bank conducts a property valuation. The purpose is to verify the current market value and ensure the loan amount aligns with the Loan-to-Value (LTV) ratio permitted by UAE Central Bank regulations.

5. Mortgage Approval

Upon successful verification of documents, valuation, and compliance with bank policies, the mortgage is officially approved. The approved amount is typically based on 50–65% of the property value, depending on buyer nationality, property type, and whether it is a first or second property purchase.

6. Disbursement

Funds are released directly to the developer as the construction progresses according to agreed milestones. Buyers do not receive the funds themselves, and payments are strictly tied to project completion stages, which ensures security for both parties.

7. EMI Begins

Buyers start paying monthly installments (EMIs) only after the bank has disbursed the funds. This often occurs after the mid-construction milestone, making it easier for buyers to manage cash flow until the property is completed.

Loan-to-Value (LTV) Ratios for Off-Plan Property in Dubai

Understanding Loan-to-Value (LTV) ratios is crucial when applying for an off-plan property mortgage in Dubai. The LTV ratio determines the maximum percentage of the property value that banks are willing to finance, with the remaining amount required as a down payment from the buyer. These regulations are set by the UAE Central Bank to ensure financial stability and reduce lending risks.

For Expatriates

-

Maximum LTV: Up to 50% of the property value

-

Buyer Contribution: At least 50% must be paid from personal funds

Expat buyers are required to provide a higher down payment due to increased risk factors, making financial planning essential before applying for an off-plan mortgage.

For UAE Nationals

-

Maximum LTV: Up to 60–65%, depending on the bank and project

UAE nationals benefit from slightly higher financing limits, reflecting lower perceived risk and government-backed financial stability programs.

For Second Properties

-

LTV ratios are typically lower, as banks view additional properties as higher-risk investments.

-

Buyers may need to provide a larger down payment or meet stricter income and credit requirements.

Key Considerations

-

LTV percentages may vary based on the bank, developer, and project type.

-

Projects from bank-approved developers often have more favorable LTV limits.

-

Buyers should plan for the down payment and associated fees, including DLD registration fees, mortgage processing fees, and agency commissions, which are not included in the LTV calculation.

Eligibility Criteria for Off-Plan Mortgages

Before approving an off-plan property mortgage, banks in Dubai carefully assess the financial stability, creditworthiness, and overall eligibility of the buyer. Meeting these criteria not only increases the likelihood of mortgage approval but also helps secure better interest rates and financing terms. Below is a detailed overview of the key eligibility requirements:

1. Income Requirements

Banks evaluate the applicant’s income to ensure they can comfortably service the mortgage. Typical requirements include:

-

Employees: Minimum monthly salary between AED 8,000–15,000, depending on the bank and property value.

-

Self-Employed/Business Owners: Must demonstrate stable business revenue, often requiring audited financial statements and higher income thresholds to meet bank risk assessment standards.

2. Employment Stability

-

Applicants must have a minimum of 6–12 months of employment with their current employer, or consistent business operations for self-employed individuals.

-

Stable employment or business history reassures banks about the borrower’s ability to make timely mortgage payments.

3. Credit Score

-

A healthy Al Etihad Credit Bureau (AECB) score of 650+ is generally preferred.

-

A strong credit score demonstrates a history of financial discipline, which increases approval chances and can lead to lower interest rates.

4. Age Limit

-

Most banks require buyers to be between 21–65 years old at the time of application.

-

Self-employed or business-owner applicants may be allowed up to 70 years, depending on bank policy and repayment plan.

5. Developer Approval

-

Off-plan mortgages are only available for projects listed with bank-approved developers.

-

Working with a reputable, bank-approved developer ensures lower risk of delays or project cancellations, which is a critical factor for mortgage approval.

Additional Considerations

-

Debt-to-Income Ratio: Banks assess existing loans and financial commitments to ensure the applicant can handle additional mortgage payments.

-

Down Payment Readiness: Buyers must be prepared to cover the required upfront payment, typically 40–50% for expats.

-

Documentation: Complete financial and identification documents are essential for a smooth approval process.

Documents Required for Off-Plan Property Mortgage

To ensure a smooth and successful off-plan mortgage application, banks in Dubai require a complete set of documents that verify the buyer’s identity, income, employment, and financial stability. Preparing all necessary documentation in advance can significantly speed up the approval process and reduce potential delays.

For Employees

Employees applying for an off-plan mortgage typically need to provide:

-

Passport Copy: Valid passport for identification purposes.

-

Emirates ID: Required for residency verification.

-

Visa Copy: Employment or residency visa to confirm legal status in the UAE.

-

Salary Certificate: Issued by the employer, detailing the monthly income and employment status.

-

Pay Slips: Usually the last 3 months to verify regular income.

-

Bank Statements: 3–6 months of statements showing salary deposits and financial stability.

For Self-Employed / Business Owners

Self-employed individuals or business owners need to provide additional documents to demonstrate business stability and income:

-

Trade License: Valid license confirming the legal operation of the business.

-

Memorandum of Association (MOA): Ownership and partnership details of the business.

-

Audited Financial Statements: Typically the last 1–2 years to verify revenue and profitability.

-

Bank Statements: 6–12 months showing consistent business and personal cash flow.

-

Passport & Emirates ID: Required for identity and residency verification.

Additional Notes

-

Some banks may request additional documents depending on the mortgage amount, nationality, or property type.

-

Ensuring all documents are up-to-date, accurate, and complete can help secure faster mortgage approval and better interest rates.

-

Working with a bank-approved developer also ensures smoother documentation and verification processes.

Benefits of Off-Plan Mortgages

Investing in an off-plan property through a mortgage offers several advantages, making it an attractive choice for both end-users and investors. From financial flexibility to modern living features, off-plan mortgages provide a structured and strategic approach to property investment.

1. Better Financial Planning

One of the main benefits of an off-plan mortgage is the ability to spread payments over several years. Instead of paying the full property cost upfront, buyers can manage construction-linked installments, making it easier to budget and maintain liquidity for other investments or personal needs.

2. Lower Monthly Installments

Monthly payments—or EMIs—only begin after the bank disburses funds, usually once the project reaches mid-construction. This allows buyers to defer major expenses during the early stages of the project, reducing financial pressure and enabling better cash flow management.

3. Higher Return on Investment (ROI)

Off-plan properties often experience capital appreciation during the construction phase, allowing buyers to secure a property at a lower launch price. Once completed, these units typically generate higher resale values and rental yields, enhancing long-term ROI for investors.

4. Modern Amenities

Off-plan developments in Dubai are designed with the latest smart home systems, energy-efficient designs, and premium community facilities. Buyers benefit from modern living standards, sustainable building practices, and access to landscaped parks, gyms, swimming pools, and retail outlets—all included in the development.

5. Lower Maintenance Costs

Newly constructed off-plan units are often covered by developer warranties, minimizing repair and maintenance expenses in the first few years. Buyers enjoy a hassle-free living experience compared to older properties, reducing long-term costs and safeguarding property value.

6. Strategic Investment Flexibility

With an off-plan mortgage, buyers can also plan for post-handover payment schemes, allowing flexibility to pay the remaining balance after moving in or renting the property. This combination of financial planning, deferred payments, and potential appreciation makes off-plan mortgages one of the most strategic ways to invest in Dubai real estate

Risks Associated with Off-Plan Mortgages

While off-plan property mortgages offer numerous benefits, it’s essential for buyers to understand the potential risks involved. Being aware of these risks helps investors and homeowners make informed decisions and implement strategies to mitigate them.

1. Construction Delays

One of the most common risks is project delays, which can postpone the handover of the property. This may impact buyers planning to move in or generate rental income. Delays can occur due to financial issues, labor shortages, regulatory approvals, or unforeseen circumstances, emphasizing the importance of choosing reputable developers with a strong delivery track record.

2. Market Fluctuations

Property prices in Dubai can rise or fall during the construction period, depending on market trends, supply-demand dynamics, and economic conditions. Buyers may experience capital appreciation or depreciation between booking and handover, making market research and timing of investment critical for maximizing returns.

3. Mortgage Rule Changes

Banks may revise interest rates, loan-to-value (LTV) limits, or eligibility criteria during the construction period. Buyers relying on variable-rate mortgages could see their repayment amounts increase, and changes in regulations may affect financing availability. Staying informed about Central Bank updates and working with mortgage-savvy advisors can mitigate this risk.

4. Developer-Related Risks

Investing in off-plan properties involves relying on the developer’s reputation and financial stability. Lesser-known or unproven developers may face delays, legal issues, or, in rare cases, project cancellations. Always verify the developer’s track record, completed projects, and bank approvals before committing to any off-plan purchase.

5. Additional Considerations

-

Changing personal circumstances: Job changes, relocation, or financial emergencies can impact repayment ability.

-

Liquidity risks: Since off-plan investments tie up capital, buyers must plan for emergencies or unexpected costs.

By understanding these risks and taking preventive measures—such as choosing reputable developers, securing bank-approved projects, and staying informed about market trends—buyers can navigate off-plan mortgages safely and make profitable long-term investments.

Interest Rates for Off-Plan Mortgages in Dubai (2026)

When considering an off-plan property mortgage in Dubai, understanding current interest rates is crucial for budgeting and calculating potential returns on investment. Mortgage rates in Dubai vary depending on the bank, loan type, property value, and prevailing economic conditions.

Average Market Rates (2025)

-

Fixed-Rate Mortgages: Typically range between 3.99% and 5.25% per annum. Fixed rates offer stability, as monthly repayments remain the same throughout the agreed period, protecting buyers from market fluctuations.

-

Variable-Rate Mortgages: Usually calculated as EIBOR + bank margin, meaning monthly installments may fluctuate according to the Emirates Interbank Offered Rate (EIBOR). This option can be beneficial when interest rates are stable or expected to decrease.

-

Islamic Mortgages (Sharia-Compliant): Operate on a profit rate structure similar to conventional loans, where the bank and buyer agree on a profit margin instead of interest. These products are widely available for off-plan property financing.

Factors Affecting Interest Rates

Mortgage rates in Dubai are influenced by both global and local financial conditions, including:

-

Global economic trends and inflation rates

-

Central Bank policies in the UAE

-

EIBOR fluctuations

-

Bank-specific lending criteria and risk assessment

Choosing the Right Mortgage Type

-

Buyers seeking predictable monthly payments may prefer fixed-rate mortgages.

-

Investors looking for potentially lower early-stage rates may opt for variable-rate mortgages.

-

For Sharia-compliant financing, Islamic mortgages offer ethical investment options while complying with Islamic banking principles.

By carefully evaluating interest rates and their potential impact on monthly payments, buyers can select the most suitable off-plan mortgage that aligns with their financial goals and investment strategy.

Best Banks Offering Off-Plan Mortgages

Selecting the right bank is a crucial step in securing an off-plan property mortgage in Dubai. Banks vary in interest rates, repayment structures, and eligibility criteria, so choosing a reliable and competitive lender can significantly impact your investment returns and financial planning. Below are some of the top banks offering off-plan mortgages in 2025:

1. Emirates NBD

-

Offers both fixed and variable-rate mortgages

-

Competitive interest rates and flexible payment options

-

Strong experience with off-plan projects from major developers

2. Mashreq Bank

-

Known for construction-linked financing and customizable payment plans

-

Offers Sharia-compliant Islamic mortgage products

-

Works closely with bank-approved developers

3. Abu Dhabi Commercial Bank (ADCB)

-

Provides attractive fixed and variable rates

-

Experienced in off-plan mortgages for both expats and UAE nationals

-

Flexible repayment terms linked to construction milestones

4. RAKBANK

-

Offers affordable down payments and staged financing

-

Quick approval process for bank-approved off-plan projects

-

Competitive rates for both conventional and Islamic mortgages

5. Dubai Islamic Bank (DIB)

-

Provides Sharia-compliant off-plan mortgage solutions

-

Profit rates comparable to conventional interest rates

-

Strong presence in Dubai’s off-plan real estate sector

6. Abu Dhabi Islamic Bank (ADIB)

-

Offers Islamic finance options with flexible repayment structures

-

Works with a wide range of developers for off-plan projects

-

Competitive profit rates and stage-linked disbursements

7. HSBC UAE

-

International bank with expertise in mortgage financing for expats

-

Offers both fixed and variable-rate options

-

Provides tailored solutions for high-value off-plan properties

8. Standard Chartered

-

Flexible mortgage options for first-time buyers and investors

-

Provides competitive rates and international financial advisory services

-

Partnered with multiple bank-approved off-plan projects

Choosing the Right Bank

When selecting a bank for your off-plan mortgage, consider:

-

Interest rates and type of mortgage (fixed, variable, Islamic)

-

LTV limits and down payment requirements

-

Processing speed and approval efficiency

-

Developer partnerships and project approval list

Working with a bank that has experience in off-plan financing ensures smooth disbursement, lower risks, and a better overall investment experience.

Tips to Get Fast Mortgage Approval

Securing an off-plan property mortgage quickly and smoothly requires preparation, financial discipline, and strategic planning. Following these best practices can significantly increase your chances of fast approval and favorable loan terms:

1. Maintain a High AECB Credit Score

-

A strong Al Etihad Credit Bureau (AECB) score, preferably 650+, demonstrates financial reliability to banks.

-

Avoid missed payments on loans, credit cards, or utilities, as late payments can slow down the approval process or reduce the loan amount.

2. Avoid Late Credit Card Payments

-

Timely credit card repayments show responsible financial behavior and improve bank confidence.

-

Avoid maxing out credit cards or taking multiple short-term loans before applying for a mortgage.

3. Choose Developer-Approved Projects

-

Banks only approve mortgages for bank-approved developers and projects.

-

Selecting an approved project ensures faster processing, smoother disbursements, and lower risk of delays or cancellations.

4. Keep All Financial Documents Updated

-

Maintain up-to-date salary certificates, bank statements, audited financials (for self-employed), and identification documents.

-

Having all required documentation ready reduces verification delays and accelerates approval.

5. Avoid High Debt-to-Income Ratios

-

Banks evaluate your existing financial obligations relative to income.

-

Keep debt-to-income ratios within recommended limits to demonstrate repayment capacity and improve the likelihood of approval.

6. Additional Tips

-

Apply during stable interest rate periods to lock in favorable mortgage terms.

-

Work with a mortgage consultant or real estate agent familiar with off-plan financing to streamline documentation and bank coordination.

-

Consider pre-approval to gauge eligibility and speed up final loan processing once construction milestones are met.

By following these tips, buyers can maximize efficiency, reduce delays, and secure an off-plan mortgage in Dubai with minimal hassle, ensuring a smoother investment experience.

Conclusion

An off-plan property mortgage in Dubai remains one of the most strategic ways to invest in the city’s dynamic real estate market. It provides buyers with lower entry prices, flexible construction-linked payment plans, and the potential for significant capital appreciation. With careful planning, an understanding of eligibility criteria, loan-to-value limits, and bank requirements, investors and homeowners alike can confidently secure a future-ready property that aligns with both lifestyle needs and long-term financial goals.

Navigating off-plan mortgages requires expertise, from choosing the right developer to selecting the most suitable bank and mortgage type. For professional assistance, personalized mortgage guidance, and access to exclusive off-plan property deals across Dubai, BS International Properties offers top-tier real estate advisory services. Their experienced team ensures that every investor or homebuyer makes smart, informed, and profitable decisions in the UAE property market.